-

Hey Guest. Check out your NeoGAF Wrapped 2025 results here!

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Nintendo Q4 results - Switch 2 tops 19.86M shippments, Switch 155.92M

- Thread starter Baemono

- Start date

Robb

Gold Member

Last edited:

Fabieter

Member

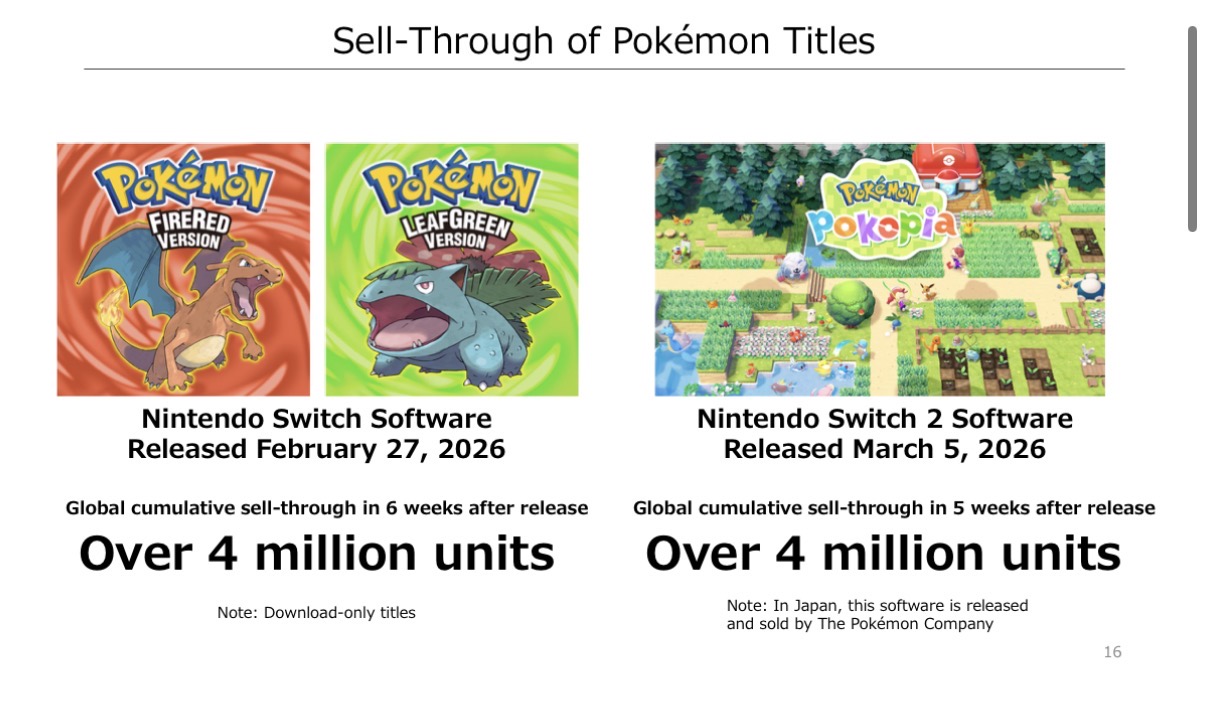

Holy shit at Tomodachi Life?

In another thread someone shitted on saros because it sold less than tomodachi life in the uk. Told him it's huge though.

Good numbers all around. I hope the stock will recover now

mèx

Gold Member

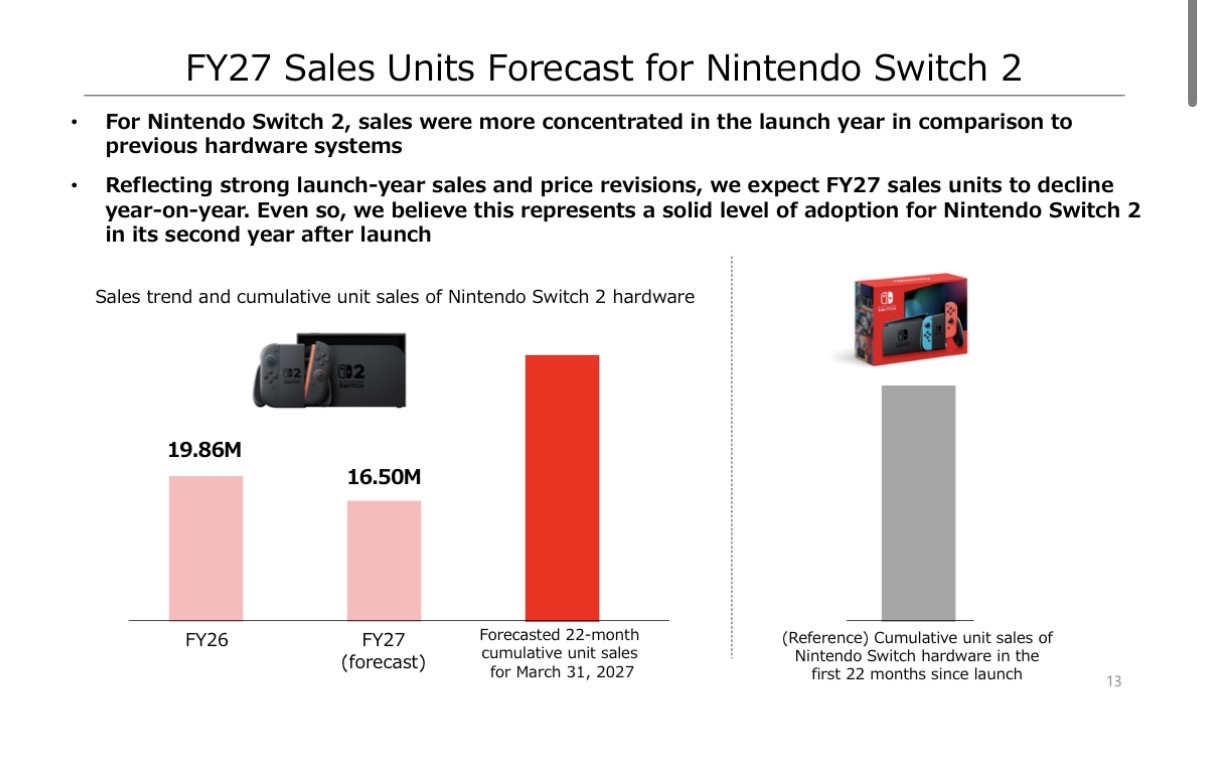

20M is a massive results, holy shit. But now they are predicting a decline in sales this year? Damn, bell curve be damned.

At this point I don't think Switch 1 will reach PS2 lifetime sales in ~2 years, it will take much more. I think Nintendo will still keep the Switch 1 around since it could be seen as the cheaper option to get into the Nintendo ecosystem. In Japan it's still selling decently well for a console that old, not sure in the West.

At this point I don't think Switch 1 will reach PS2 lifetime sales in ~2 years, it will take much more. I think Nintendo will still keep the Switch 1 around since it could be seen as the cheaper option to get into the Nintendo ecosystem. In Japan it's still selling decently well for a console that old, not sure in the West.

Last edited:

Robb

Gold Member

So with the updated yearly forecast Switch 2 should land at 36M units shipped by 31 March 2027.

Absolutely crazy that they've managed to sell 20M units in only 10 months, especially given that the original forecast was "only" 15M.

Looks like things will start going back to 'normal' from here though.

Absolutely crazy that they've managed to sell 20M units in only 10 months, especially given that the original forecast was "only" 15M.

Looks like things will start going back to 'normal' from here though.

Baemono

Gold Member

I was like « who the hell bought these »4m sales for a Pokemon rom at £15 a pop gives me hope that they won't leave Ruby/Sapphire/Emerald on the table.

And then I recalled I did

They missed the 21m forecast.

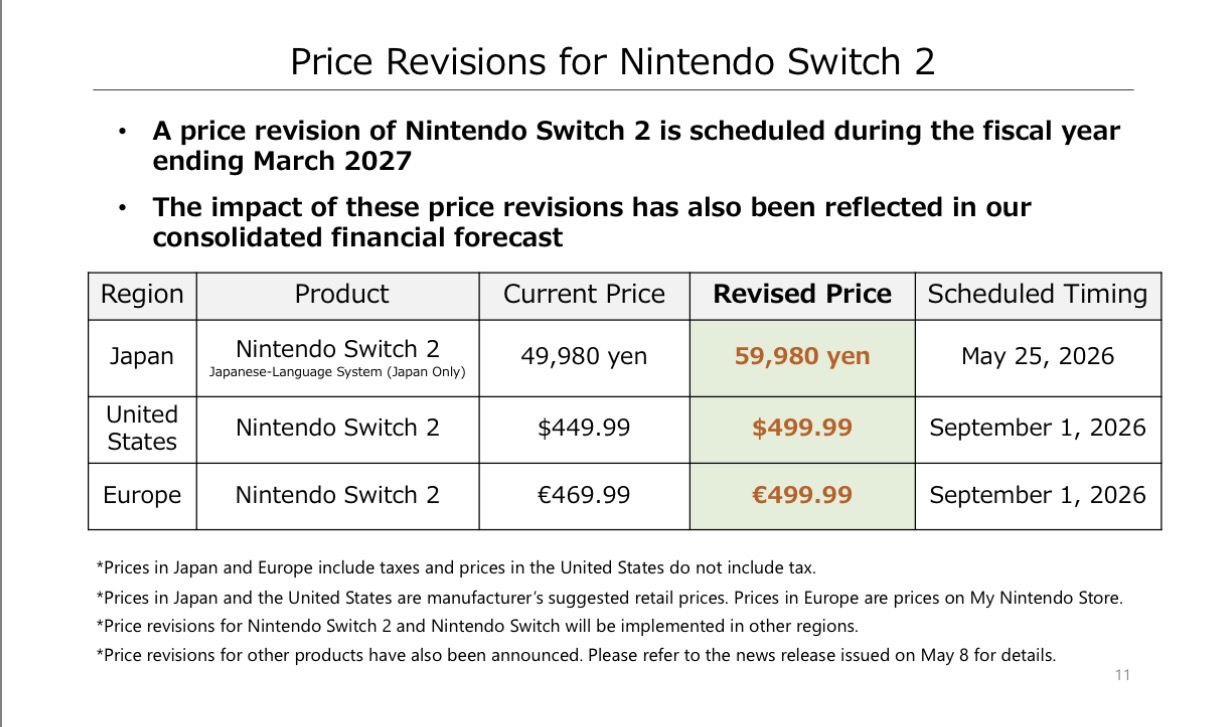

They forecast 16.5m units this year, a decline which in year two of a system liifecycle is very unusual but can be explained with the price increase (oh well now it seems some peole will change the tune from "you only do it if you're greedy") plus not expecting huge holiday season titles.

Not particularly good.

They forecast 16.5m units this year, a decline which in year two of a system liifecycle is very unusual but can be explained with the price increase (oh well now it seems some peole will change the tune from "you only do it if you're greedy") plus not expecting huge holiday season titles.

Not particularly good.

Last edited:

Robb

Gold Member

The revised forecast was 19M units. They beat it by ~1M.They missed the 21m forecast.

They forecast 16.5m units this year, a decline which in year two of a system liifecycle is very unusual but can be explained with the price increase (oh well now it seems some peole will change the tune from "you only do it if you're greedy") plus not expecting huge holiday season titles.

Not particularly good.

J Required

Banned

Only 16m this year? Thats unusually low forecast for console this new.

Also Ninty basically confirmed what I have been saying since last September in the second slide.

How much did Switch 2 sell for the quarter?

Also Ninty basically confirmed what I have been saying since last September in the second slide.

How much did Switch 2 sell for the quarter?

Last edited:

Robb

Gold Member

Agreed, although it might be intentionally conservative. They missed the mark on their initial Switch 2 forecast for this year by roughly 5M units.Only 16m this year? Thats unusually low forecast for console this new.

Baemono

Gold Member

The were forcasting 19 millionThey missed the 21m forecast.

Robb

Gold Member

They shipped an additional 2.49M this quarter.How much did Switch 2 sell for the quarter?

NeoIkaruGAF

Gold Member

It has basically topped the reported sales of PS2 before the notorious revision. Not bad for a system that people predicted to be DOA.Its like they don't want the Switch to topple the PS2 lifetime sales figure, especially with the new price hike.

And with the Switch 2's imminent price hike, who knows, the old Switch may still be squeezed for a little more juice.

J Required

Banned

It has basically topped the reported sales of PS2 before the notorious revision. Not bad for a system that people predicted to be DOA.

And with the Switch 2's imminent price hike, who knows, the old Switch may still be squeezed for a little more juice.

Here we go again!!! Cope

cafecat

Member

Investors now are not really interested in game company, if any of these investors put some of their money on Intel stock early this year, the return of investment would be way impressive. There are still lot of stock has potential like Intel than game company, investors are going to arrange less money on game company.In another thread someone shitted on saros because it sold less than tomodachi life in the uk. Told him it's huge though.

Good numbers all around. I hope the stock will recover now

It may has some recover but still far away from its peak: consider the cost of components, re-normalization of pandemic bloom of video game industry, the higher price tag, consumer economy and e.t.c.., Nintendo need some service like PS plsu sub to provide constant revenue to let more investor prefer its stock.

NeoIkaruGAF

Gold Member

Yes dear, by all means go on seeing console warriors everywhere.Here we go again!!! Cope

J Required

Banned

What? You basically refused to believe Sony reported numbers because you didn't like what it says. Call Nintendo and tell them to pump Switch numbers then ..Yes dear, by all means go on seeing console warriors everywhere.

")

ShaiKhulud1989

Gold Member

Forecast slump is looking grim. Basically no 2026 titles to push the system on a wider audience.

J Required

Banned

Switch 2 basically sold 10m in few days then the momentum slowed down and even Nintendo acknowledges that for next year.

Baemono

Gold Member

Still not its full first year though, but that's irrelevant.20m in its first year is pretty impressive.

DenchDeckard

Moderated wildly

Switch 2 doing well. If they announce a full ocarina of time remake......Holy shit.

Last edited:

Steve Holt

Member

The amount of remakes and remasters they are doing man..

Please show us a new Mario.

Please show us a new Mario.

DenchDeckard

Moderated wildly

So the switch needs to sell another 5 million to beat the PS2?

What are the chances? - Surely it can do it in one more year?

What are the chances? - Surely it can do it in one more year?

J Required

Banned

What are the revenues and profit like? OP you slacking

cafecat

Member

revenue and profit are up as switch 2 release and new games, but the metric related to margin are downWhat are the revenues and profit like? OP you slacking

| Metric | FY2026 actual | FY2025 actual | YoY change |

| Revenue (net sales) | ¥2,313.1bn | ¥1,164.9bn | 98.60% |

| Operating profit | ¥360.1bn | ¥282.6bn | 27.50% |

| Ordinary profit | ¥542.2bn | ¥372.3bn | 45.60% |

| Profit attributable to owners of parent | ¥424.1bn | ¥278.8bn | 52.10% |

| Operating margin | 15.60% | 24.30% | -8.7 pt. |

| Net margin | 18.30% | 23.90% | -5.6 pt. |

Investor concerning factors:

| Investor concern | Why it matters |

| Margin deterioration | Revenue nearly doubled, but operating margin fell sharply from 24.3% to 15.6% |

| Weak FY2027 guidance | Nintendo forecast only ¥370bn operating profit vs analyst expectations around ¥480bn |

| Switch 2 profitability pressure | Hardware appears to have much lower margins, possibly near breakeven or loss-leading |

| Price hikes may hurt demand | Nintendo is raising Switch 2 prices globally amid inflation/tariff pressure |

| Unit sales guidance disappointed | Forecast Switch 2 sales of 16.5m units is below many analyst expectations |

| Costs are rising fast | Memory prices, tariffs, logistics, and components are hurting profitability |

| Advertising expenses surged | Marketing spend jumped 67% YoY |

| Profit quality questions | Part of net profit came from FX gains and investment-security sales rather than core operations |

Last edited:

Fabieter

Member

Investors now are not really interested in game company, if any of these investors put some of their money on Intel stock early this year, the return of investment would be way impressive. There are still lot of stock has potential like Intel than game company, investors are going to arrange less money on game company.

It may has some recover but still far away from its peak: consider the cost of components, re-normalization of pandemic bloom of video game industry, the higher price tag, consumer economy and e.t.c.., Nintendo need some service like PS plsu sub to provide constant revenue to let more investor prefer its stock.

It will nintendo and sony are really cheap right now.

J Required

Banned

"Switch 2 profitability pressureHardware appears to have much lower margins, possibly near breakeven or loss-leading"

Nvidia typical d***

Burned MS with OG Xbox, Burned Sony with PS3 and now experimenting with Nintendo!

Nvidia typical d***

Burned MS with OG Xbox, Burned Sony with PS3 and now experimenting with Nintendo!

They fell just shy of their raised 20M Switch 2 sales target for March. Depends how the market reacts to that. Software they're doing better though so hopefully it goes up.Good numbers all around. I hope the stock will recover now

Last edited:

LordOcidax

Member

I totally forgot about this last night…. But.

efyu_lemonardo

May I have a cookie?

That's not necessarily the case. There may be a hardware/manufacturing bottleneck limiting Switch 2 sales. And Nintendo may have adjusted their release schedule accordingly.they are basically confirming there's no big holiday title, no mario animal crossing or Smash.

Seems very dire tbh. I don't get how they had so much time to prepare for this and still failed.

Last edited:

LordOcidax

Member

They beat the 19M forecast, by almost 1M.They always lowball the forecasts, specially after missing the previous one. They'll adjust by rising it up later.

J Required

Banned

You meant that they didn't reach their revised forcast of 20m unit, also forcasting 16.5m for next year.They beat the 19M forecast, by almost 1M.

I think the price increase is taken into account as well.That's not necessarily the case. There may be a hardware/manufacturing bottleneck limiting Switch 2 sales. And Nintendo may have adjusted their release schedule accordingly.

Robb

Gold Member

They never made a revised forecast to 20M.You meant that they didn't reach their revised forcast of 20m unit, also forcasting 16.5m for next year.

The Q1 estimate was 15M. In Q2 they revised it up to 19M. In Q3 they maintained the 19M estimate. In Q4 they beat it by 1M.

efyu_lemonardo

May I have a cookie?

Definitely. The price increase reflects manufacturing difficulties, such as the competition over procuring RAM.I think the price increase is taken into account as well.

Last edited: